Introduction to Credit Scores

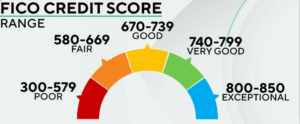

A credit score is a crucial number that reflects your financial habits and reliability as a borrower. Lenders, landlords, and even some employers use this score to gauge how likely you are to meet your financial obligations. Ranging typically from 300 to 850, your credit score is calculated based on several factors, such as your payment history, total debt, credit age, types of credit, and recent inquiries. Each of these components plays a role in shaping your financial profile and determining how trustworthy you appear to potential creditors.

In the United States, the credit system is built to provide a standardized method of evaluating financial risk. The importance of credit scores extends far beyond loan approvals; they also impact the terms you receive, such as interest rates and credit limits. The higher your score, the better the terms you can usually secure. While credit scores may feel like just another number, they can significantly shape your financial journey.

As the way we manage money becomes increasingly digital, the tools and methods for assessing creditworthiness are also advancing. Monitoring your credit score and understanding the factors that affect it are now easier than ever, thanks to various apps and services offering real-time updates and insights. Being proactive about your credit score allows you to spot areas for improvement and take action to build a stronger financial standing.

Changes in Credit Scoring by 2025

The credit scoring system in 2025 incorporates advancements aimed at providing a more accurate and inclusive assessment of financial behavior. Unlike traditional models that rely heavily on payment history and existing debts, newer methods evaluate additional data sources, including consistent payment of utility bills and rent. These changes reflect an effort to capture a broader range of financial activities, offering individuals with limited credit history an opportunity to demonstrate their reliability.

Technological innovation plays a central role in reshaping credit evaluations. Artificial intelligence and machine learning are increasingly being used to analyze complex data patterns, allowing for more precise and fair assessments. These tools can identify trends in financial behavior that traditional scoring methods might overlook. For instance, small yet consistent payments toward non-traditional obligations can now contribute positively to a person’s overall credit profile.

In addition to changes in the data being used, 2025 brings shifts in how consumers access and interact with their credit information. Real-time monitoring tools are now more robust, providing consumers with detailed insights into their financial habits and how these impact their credit scores. This greater transparency empowers individuals to take immediate action when necessary, such as addressing negative trends or fixing errors on their credit reports.

Regulatory changes have also encouraged the development of scoring systems that reduce disparities and make credit evaluations more equitable. By considering alternative data points, these updated models aim to address long-standing challenges, such as the difficulty faced by young adults or immigrants in establishing credit under traditional systems. The evolution of these systems reflects a broader shift toward fairness and inclusivity in financial evaluations.

Partnerships between technology companies, financial institutions, and regulators have been instrumental in driving these advancements. New platforms are emerging that allow consumers to connect their financial accounts securely, providing a complete picture of their financial health while maintaining strong privacy protections. This collaboration between various stakeholders ensures that innovations in credit scoring benefit both consumers and lenders.

Why Credit Scores Are Critical in 2025

In 2025, credit scores hold more weight than ever before in shaping an individual’s access to financial resources. They serve as a primary tool for lenders to measure financial responsibility and assess the risk of lending money or extending credit. This means that your credit score directly influences not only whether you qualify for financial products but also the terms offered to you. A stronger credit score can unlock more favorable loan conditions, including reduced interest rates and higher credit limits, which can result in significant long-term savings.

The importance of credit scores is not limited to traditional lending. In today’s interconnected financial landscape, companies offering innovative payment solutions or buy-now-pay-later options also rely on credit data to make decisions about extending services. As financial systems adapt to new technologies and consumer behaviors, the role of credit scores has expanded beyond banks to include fintech firms and alternative lenders.

With the rise of integrated financial platforms in 2025, consumers are encouraged to take a more active role in monitoring and improving their credit. Credit scores no longer exist solely as a static evaluation tool; they now serve as a dynamic reflection of how individuals manage their overall financial health. Companies offering real-time monitoring and predictive insights make it easier for people to understand how their daily financial decisions impact their creditworthiness, reinforcing the need for responsible habits.

Credit scores also play a pivotal role in fostering trust between parties. For instance, landlords and property management companies frequently review credit scores to evaluate a potential tenant’s reliability in paying rent. This makes a strong credit score a key factor in securing housing opportunities. Additionally, insurance providers often factor in credit scores when setting rates, further emphasizing their reach into essential aspects of daily life.

The push for financial inclusivity in recent years has driven changes in how credit scores are calculated, ensuring that more people can benefit from having their financial behavior accurately assessed. While these developments aim to make credit evaluations more equitable, individuals must remain proactive in understanding and managing their credit. By prioritizing financial literacy and taking advantage of advanced tools to track progress, consumers can harness the full potential of their credit scores in the evolving financial landscape of 2025.

Impact on Personal and Professional Life

Your credit score influences various aspects of your daily life beyond borrowing money. In the workplace, some employers include credit checks in their hiring processes, especially for roles involving financial responsibilities. A strong credit profile can create a positive impression, while a lower score might raise concerns about reliability. Similarly, in housing, landlords often evaluate credit scores to assess whether potential tenants can reliably pay rent. This can determine whether your application is accepted or denied, particularly in competitive rental markets.

Insurance companies also factor in credit scores when calculating premiums for auto and home insurance. A higher score can lead to lower rates, while a lower score may result in higher costs. These practices are based on studies showing a connection between credit behavior and the likelihood of filing insurance claims. The widespread use of credit scores in determining essential services like housing and insurance highlights their impact on your financial stability.

In addition to affecting access to housing and employment, credit scores play a role in expanding opportunities for personal and professional growth. For instance, securing financing for education or professional development often requires a credit check. A strong score may help you qualify for loans with better terms, making it more affordable to pursue higher education or specialized training. On the flip side, a weaker score could limit your options or lead to higher borrowing costs.

Furthermore, as financial technologies continue to evolve, more services rely on credit data for decision-making. Subscription-based programs, installment plans, and other flexible payment solutions often assess creditworthiness as part of their approval process. This means your credit score can determine whether you gain access to these conveniences, which are becoming increasingly integrated into daily life.

While the credit scoring system is designed to reflect financial behavior, its influence extends far beyond financial transactions. As technology and data usage grow, your credit profile has become an essential factor in evaluating your dependability and trustworthiness across different sectors.

Tips to Improve Your Credit Score

Taking proactive steps to enhance your credit score starts with developing consistent habits that showcase financial responsibility. One effective strategy is setting up automatic payments to ensure bills are always paid on time, avoiding the negative impact of missed or late payments. Prioritizing high-interest debt can also be beneficial, as it reduces your overall financial burden while improving your credit utilization ratio.

Managing your credit utilization is another key factor. This means keeping the balance on your credit cards below 30% of your total credit limit, as high utilization can signal financial strain to lenders. If possible, aim for even lower usage, as it demonstrates careful management of available credit.

Another useful approach is to maintain older credit accounts, even if they’re not in active use. The age of your credit accounts contributes to your overall score, so closing long-standing accounts may inadvertently lower it. Additionally, when applying for new credit, be selective to avoid multiple hard inquiries within a short timeframe, which can temporarily decrease your score.

Building a diverse credit portfolio can also have a positive impact. Balancing different types of accounts, such as credit cards, auto loans, and student loans, shows creditors that you can manage various financial obligations responsibly. However, it’s essential to take on new credit only when necessary and within your financial means.

Regularly reviewing your credit reports is a vital habit. Errors, such as incorrect account balances or payments marked late by mistake, can harm your score if left unaddressed. Federal law allows you to request a free credit report annually from the three major credit bureaus, making it easier to spot discrepancies and dispute them quickly.

For those with limited or no credit history, exploring alternative options like secured credit cards or becoming an authorized user on a trusted individual’s account can help establish or improve credit. These tools allow you to demonstrate responsible usage without taking on excessive risk.

Lastly, engaging with credit-building tools or programs can offer tailored strategies for improving your score. Some services analyze your financial behavior and recommend specific actions to strengthen your credit profile, making it easier to work toward your goals systematically. Consistency and informed decision-making are key to achieving lasting improvements.

Conclusion and Future Outlook

Looking ahead, the role of credit scores in shaping financial opportunities will continue to expand, highlighting the importance of maintaining a strong credit profile. The credit system in the USA is evolving, with technological advancements driving greater transparency and inclusivity. These changes are making it easier for individuals to understand their credit health and take actionable steps to improve it. For many, this means embracing tools that provide real-time updates, detailed insights, and personalized strategies to manage credit more effectively.

As financial systems integrate more data sources and adopt innovative scoring methods, individuals will have access to fairer evaluations of their financial behavior. This shift aims to reduce barriers for those who may have struggled under traditional systems, such as younger people or those with limited credit histories. By recognizing a broader range of financial activities, these changes open the door to opportunities previously out of reach for many consumers.

In this evolving landscape, a proactive approach to credit management is essential. Staying informed about updates to credit scoring models and adapting to new tools can help consumers maintain a competitive edge. The increasing availability of resources that break down complex credit information into actionable advice allows individuals to build better habits and strengthen their financial standing.

As credit scores grow more intertwined with essential aspects of personal and professional life, the need for financial literacy becomes more pressing. By fostering an understanding of how daily decisions impact credit, individuals can make smarter choices that benefit them in both the short and long term. Whether through education, leveraging technology, or engaging with innovative programs, taking charge of one’s credit health is more achievable than ever.

The advancements on the horizon bring both opportunities and responsibilities. While these changes create new paths for financial growth, they also call for a greater commitment to maintaining sound financial practices. By aligning with these shifts, consumers can position themselves to thrive in an increasingly interconnected financial world.